Fixing the safety net: What next on supporting working people’s incomes?

The coronavirus pandemic poses huge risks to workers’ health, jobs and livelihoods. Following consultation with trade unions, the chancellor announced a new job retention scheme on Friday 20 March.

This report sets out what government must do next to protect family incomes (building on our report published last week). Government must now:

- guarantee incomes for self-employed people, extending the protection applied to employees to an additional five million workers

- introduce paid parental leave for parents who need to take time off work to care for children who are not attending school

- fix the sick pay system, by raising the level to the equivalent of 35 hours a week at the real living wage – just over £300 a week – and extending entitlement to an additional two million people.

What has government already announced?

What’s been announced already on supporting wages?

On Friday 22 March the chancellor announced the Coronavirus Job Retention Scheme to provide wage support to workers who are temporarily laid off – or furloughed – due to coronavirus.

All businesses are eligible, and the scheme will support everyone on a company’s payroll. This should include most zero-hours workers – though not those who are self-employed.

Government guidance sets out that businesses must:

- designate affected employees as ‘furloughed workers,’ and notify your employees of this change – changing the status of employees remains subject to existing employment law and, depending on the employment contract, may be subject to negotiation

- submit information to HMRC about the employees that have been furloughed and their earnings through a new online portal (HMRC will set out further details on the information required)

The guidance further says that HMRC will reimburse 80 per cent of furloughed workers’ wage costs, up to a cap of £2,500 per month. HMRC are working urgently to set up a system for reimbursement. Existing systems are not set up to facilitate payments to employers.

In announcing the scheme, the chancellor said that it the payments would be backdated to the 1 March, and initially available for three months. However, he said that he would extend the scheme for longer if necessary, and there would be no limit on the amount of payments. 1

The TUC believes that this scheme is a significant intervention. Employers in most industries should now use the scheme to maintain jobs. This level of support means there is no excuse for employers to make mass redundancies. Union reps should urgently open negotiations with employers about how they take advantage of the scheme and what that means for workers in practical terms.

But the scheme at present hasn’t provided protection for key groups, including the self-employed, those on sick pay, and parents who need to care for their children due to school closures.

What other support has government announced for families and businesses?

In announcing the wage subsidy, the chancellor also added to the small-scale steps taken to provide additional support to households. Taking into account the announcements in the Budget and those on March 20:

- Sick pay will now be paid from day one, rather than the fourth day of sickness (following trade union demands).

- Eligibility for universal credit has been widened, and the basic amount has been increased. Self-employed people no longer need to meet a minimum income floor in order to qualify for the benefit, and the basic amount has been increased for everyone by £1,000 a year – meaning a weekly amount of £94 a week (matching the level of statutory sick pay).

- Housing benefit has been increased, meaning that it will now provide support with rents up to the 30th percentile of rents in the local area (and reversing a change made by the coalition government in 2012).

- Government has announced a £500m hardship fund to be administered by local authorities.

- Self-employed people will not have to make a self-assessment tax payment until January 2021.

Government has also announced a package of support for businesses:

- Small businesses (with less than 250 employees) will be able to claim back the costs of two weeks’ sick pay for workers who are off for work because of coronavirus.

- There will be a 12-month business rates holiday for all retail, hospitality, leisure and nursery businesses in England.

- There will be a small business grant funding of £10,000 for all businesses in receipt of small business rate relief or rural rate relief.

- There will be grant funding of £25,000 for retail, hospitality and leisure businesses with property with a rateable value between £15,000 and £51,000.

- The Coronavirus Business Interruption Loan Scheme will offer loans of up to £5m for SMEs through the British Business Bank.

- A new lending facility from the Bank of England will help support liquidity among larger firms, helping them bridge coronavirus disruption to their cashflows through loans.

- There will be a deferral of the next VAT payment date until June 2020.

What still needs to happen?

Government support has gone some way to protect wages. But there are three important groups missing out who need assistance now.

- the self-employed

- those forced to claim sick pay and forced to cope on just £94 a week

- parents who need to stay off work in order to look after their children now schools are closed.

Supporting the self-employed

It is an urgent priority to support the more than five million self-employed people who are not covered by the government’s job retention scheme. Measures taken last week – to delay the next self-assessment tax payment and ensure that self-employed people on low incomes can access support up to £94 a week through the benefit system – are clearly inadequate.

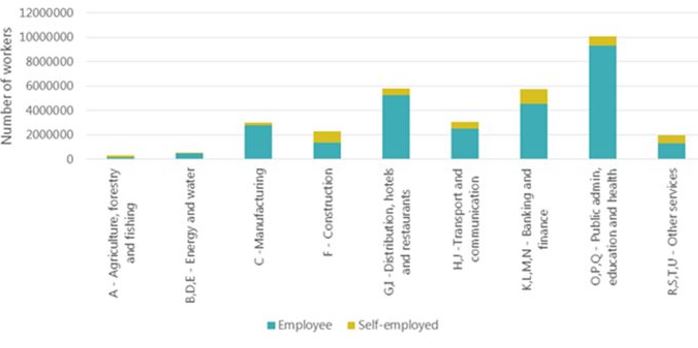

Industries with particularly high levels of self-employment include the creative industries (listed here in ‘other services’), agriculture, forestry and fishing and construction. These workers must not be left behind. See graph:

Number of workers by Industry sector (employed and self employed)

The Federation of Entertainment Unions has called for a guaranteed minimum income to support self-employed people during this period. It believes there are two ways this could be delivered – listed here in order of preference.

1) Guarantee self-employed people a significant percentage of their income based on their last three years of self-assessment income.

We believe that the most effective way to support the self-employed would be to put in place a scheme mirroring the support for employed workers, and guaranteeing at least 80 per cent of income up to a maximum of £2,500 a month.

HMRC already holds significant information about the earnings of the self-employed:

- Every self-employed person using the self-assessment must submit an annual tax return. However, this applies to the previous year’s income, so could be out of date (the deadline for self-assessment is 31 January, relating to earnings up to the 5th of April in the previous year).

- It’s also the case that self-employed people claiming universal credit must submit a monthly assessment of their income.

So, as in Norway, government could extend the job retention wage subsidy to the self-employed, paying at a rate of at least 80 per cent of income based on their previous three year’s self-assessment income.

Grant payments could then be made to self-employed people using their self-assessment tax details (in the same way a repayment would be made to someone who has overpaid tax).

Government could also consider scaling up the income assessment process used in universal credit to cover those applying to this scheme.

This would mirror schemes in other countries:

- Norway is to pay self-employed workers grants equating to 80 per cent of their average income over the past three years.

- Belgian self-employed workers will have access to an income replacement scheme.

2) Provide a flat-rate payment to all self-employed people affected by coronavirus.

An alternative approach could be to provide a flat-rate payment to all self-employed people affected by coronavirus.

We believe this should be based on the equivalent of 35 hours work at the National Living Wage, or around £320 a week.

This payment could potentially be:

- paid through the self-assessment tax system as a rebate

- paid through universal credit (although this would also require relaxation of existing rules within universal credit which exclude those with significant savings); or

- paid (as the Resolution Foundation suggests) by increasing an existing contributory benefit such as contributory jobseeker’s allowance, which does not have rules which bar those with savings from accessing it.

Ensuring that the existing job retention scheme covers as many people as possible

We believe there are some groups of workers who might be best covered by the existing job retention scheme. These include – but are not limited to:

- construction workers paid by the Construction Industry Scheme who should be covered by the coronavirus job retention scheme – even where they are paid via umbrella or payroll companies

- performers and stage management working on conventional Equity contracts up until last week's shutdown of the entertainment industry (i.e. in the West End, commercial and independent theatre, on the TV soaps, etc) who have similar characteristics to those covered by the job retention scheme – industry bodies need to receive clarity from government that this is the case.

Government should also ensure that employers are extending the protection of the job retention scheme to all workers – whatever their employment model – and clarify that its intention is to protect as many workers as possible.

Fixing sick pay

As the health minister Matthew Hancock admitted this week on Question Time, £94 a week in sick pay is too low to live on.

Government’s priority should now be to increase urgently the weekly level of sick pay from £94.25 to the equivalent of a week’s pay at the Real Living Wage.

In addition, almost two million people are not eligible for sick pay, because they earn too little to qualify. In response to this problem, the government has increased the support available via universal credit – available to people who don’t get sick pay – to £94 a week.

But claiming benefits remains complex, and some people may miss out because their savings are too high, or because their household income pushes them over the income threshold – for example due to having a partner still in work.

Government needs to act now to remove the lower earnings limit for qualification for sick pay, and ensure everyone can access it, no matter how much they earn .

Supporting parents

It is not yet clear whether the job retention scheme can be used to support parents who may need to not go to work due to school closures.

If this is not the case (given that it is linked to a reduction in business demand – rather than workers needing to be off work for other reasons), government must urgently introduce support for these workers (as we set out in our note):

- Government should introduce guaranteed paid parental leave for one primary carer for the duration of the school and nursery closures, with government reimbursement for employers.

- This must be accompanied by protection from unfair treatment or dismissal for parents who take up this leave, no matter how long they’ve worked in their jobs.

Other forms of support

With significant income drops likely, government urgently needs to design a wider package of support for households, in addition to wage subsidies and better sick pay. It should consult unions, employers and civil society on this, but measures could include:

- a fully funded freeze on council tax payments, as well as council tax debt repayments

- significantly increasing the hardship fund for local authorities, and the details clarified

- a further immediate increase in social security payments

- ending the five-week wait for universal credit

- additional support with rental costs as well as mortgages, including for those not claiming housing benefit.

Stay Updated

Want to hear about our latest news and blogs?

Sign up now to get it straight to your inbox